The Future of Liquidity Forecasting in Community Banking

From Experience-Driven Judgment to AI-Powered Precision

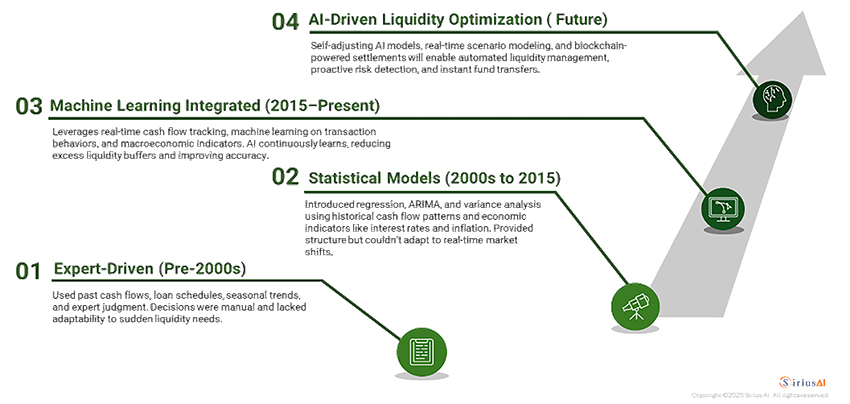

Liquidity forecasting has always been a critical function for banks, ensuring the right balance between maintaining sufficient cash reserves and optimizing capital efficiency. Historically, banks have relied on past cash flow patterns, such as daily deposit fluctuations and seasonal transaction trends, to estimate future liquidity needs. Treasury teams manually adjusted projections based on internal policies and anticipated economic shifts.

As financial markets evolved, statistical forecasting methods—such as moving averages, ARIMA models, and regression analysis—were introduced to provide a more structured approach. These models improved accuracy but still struggled to adjust dynamically to sudden changes in economic conditions and regulatory shifts

Evolution of Liquidity Forecasting

The Shortcomings of Traditional Forecasting Methods

For instance, during the 2008 financial crisis, many banks miscalculated the extent of cash outflows, leading to unexpected liquidity shortages. Similarly, the COVID-19 pandemic in 2020 saw banks, especially community banks, struggling to adjust to rapid changes in cash flow needs as businesses and consumers shifted spending behaviors overnight. These incidents highlighted the inherent limitations of traditional forecasting techniques, which relied too heavily on past trends rather than real-time market signals.

With rising regulatory expectations and increasing pressure to optimize liquidity, community banks are adopting more sophisticated methods. Machine learning and real-time forecasting capabilities are transforming treasury cash management, improving prediction accuracy and reducing reliance on emergency funding. Research highlights that AI-driven liquidity forecasting is helping community banks improve capital allocation and reduce excessive liquidity reserves, leading to better cost efficiency while ensuring regulatory compliance.

The Business Case for Smarter Liquidity Forecasting

For community banks that still rely on manual forecasting and historical data, the risks of inaccuracy are significant. Forecasting inaccuracies can lead to excess idle cash, limiting lending and investment opportunities, or unexpected shortfalls, forcing them to borrow at high rates to meet liquidity requirements. Studies on treasury risk highlight the challenges of balancing liquidity while maintaining compliance. Traditional methods often struggle to incorporate real-time economic and behavioral data, leading to costly miscalculations.

By integrating AI-driven forecasting, community banks can enhance liquidity planning, reduce emergency borrowing, and improve regulatory compliance. AI models refine accuracy, ensuring optimal cash reserves without excessive liquidity buffers.

What Lies Ahead – The Future of Liquidity Forecasting

As banking becomes more digital, liquidity forecasting shifts from historical analysis to real-time, AI-driven decision-making. This isn’t just about improving accuracy but helping community banks actively manage liquidity rather than simply predicting cash needs.

Machine learning has already improved forecasting by identifying spending patterns and cash flow trends, but AI takes this a step further by helping banks act on these insights in real time.

AI can now simulate multiple 'what-if' scenarios, such as a sudden rise in withdrawals or an interest rate hike, allowing banks to prepare in advance. Instead of relying solely on past data, AI enables treasury teams to test different possibilities and adjust liquidity plans before disruptions occur.

Community banks manage money across branches, ATMs, and corporate accounts, but balancing cash across these locations has always been a challenge. AI-powered forecasting optimizes cash distribution, ensuring ATMs are stocked accurately, branches maintain the right reserves, and extra funds don’t sit idle where they aren't needed.

Compliance with regulations like Basel III has traditionally been reactive, requiring manual reporting and adjustments. AI-driven regulatory tracking can proactively monitor policy changes and adjust liquidity buffers automatically, ensuring compliance before new rules take effect.

The Future is Data-Driven – Are Banks Ready?

For community banks accustomed to spreadsheet-driven forecasting, shifting to AI may seem like a big leap. But the transition is already happening. Tier 1 and Tier 2 financial institutions are integrating AI into treasury operations, and mid-sized and Community banks that delay adoption risk falling behind.

The good news? AI-powered forecasting is now more accessible than ever. Thanks to cloud-based AI platforms and external expertise, community banks can integrate real-time liquidity forecasting without overhauling existing infrastructure.

Rather than replacing traditional tools, AI enhances and complements existing treasury practices—making forecasting faster, more precise, and easier to manage.

The transition is happening now. The question is: Who will adapt in time?

About SiriusAI

SiriusAI provides financial institutions, payments companies, and Fintechs with AI Consulting and development of measurable outcomes with AI Solutions. SiriusAI is proud to serve multiple banks, fintechs, and other institutions across Georgia.

Learn more at www.siriusai.com